Your Cart is Empty

Apparel and textiles is big business on the world stage, and has seen some monumental changes in the last few decades. Consumers are more conscious than ever of worker’s rights and the environment as fast fashion faces off against slow fashion and sustainable fashion.Trade policy is shifting and world changing events are impacting the economy, resulting in an uncertain future for the textile and apparel industry. Certainly there’s much more detail to international trade policies, globalization, manufacturing and free market ideals than is included here, and nature and size of the industry merits more intense study for those interested.The information covered here should serve as a starting point for many and a quick reference guide to help shade in the details of how the apparel and textile industry has developed to date, and act as a weathervane for where it’s headed.

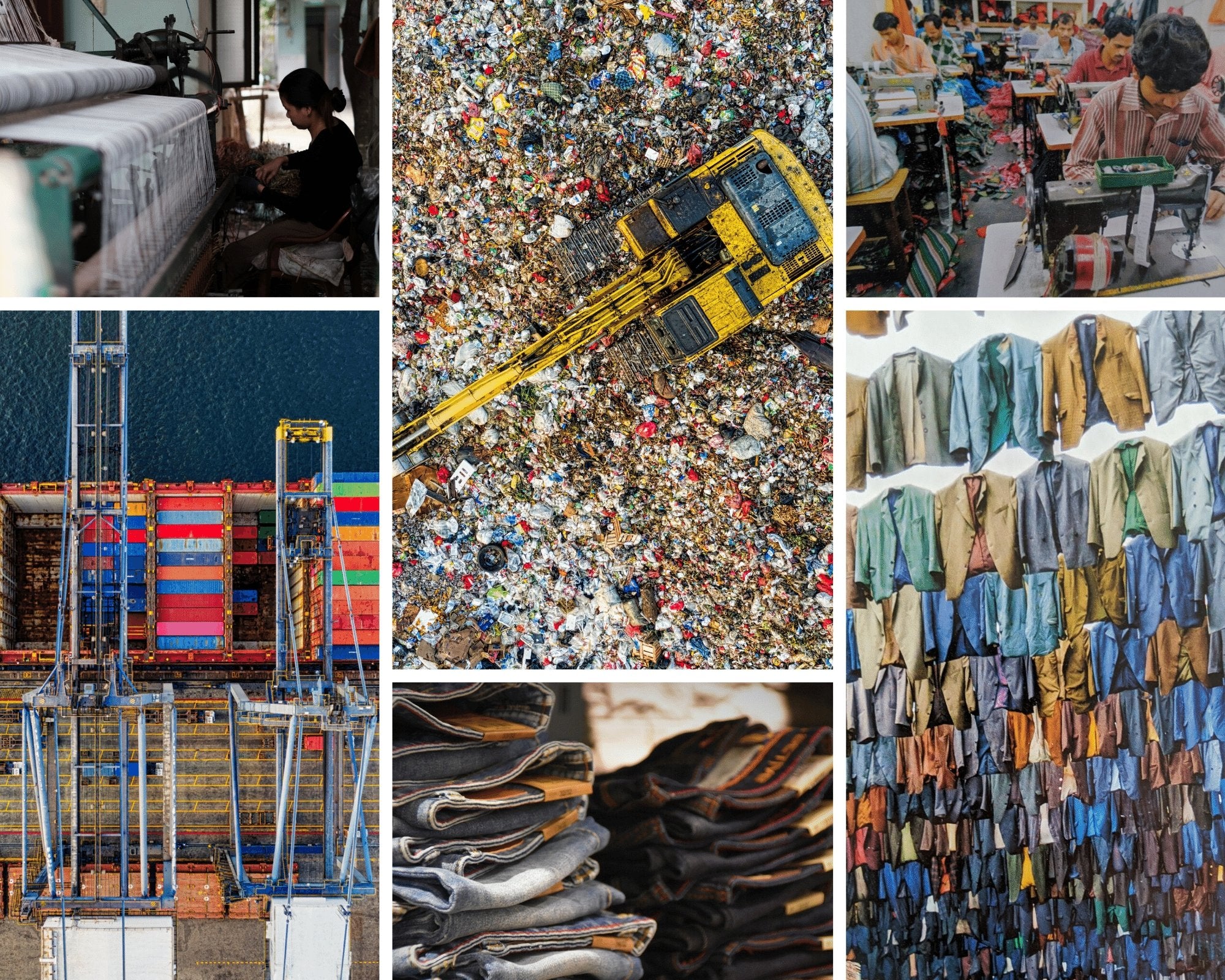

Next time you’re shopping for clothes at a big brand store check the label for country of origin. Names like Vietnam, Bangladesh, Sri Lanka and China are all safe bets for where the clothing you're looking at was manufactured. These countries in Southeast Asia have emerged as dominant players in the $450 bn textile and apparel market, many of which now dwarf the domestic output in the countries that import their goods, but it wasn’t always this way.The apparel industry today has been shaped by policies rooted in the late twentieth century and to a potentially greater extent the 2008-2009 recession.Governments have succeeded in deregulating the industry by leading with a policy of liberalized markets, forming the contemporary supply chain for what is now known as fast fashion. This new globalized economy and recent economic upheaval has served the interests of countries in Asia that enjoyed a competitive advantage as a result, and shaped the contemporary landscape of this multi-billion dollar business.

The United States and the European Union imposed trade regulations from the 1970’s to the early 2000’s, such as the Multi Fibre Agreement (MFA) and Agreement on Textiles and Clothing (ATC).These controls restricted imports from suppliers abroad such as China, Vietnam & South Korea,protecting domestic industries threatened by cheaper imported goods. The exporting countries subject to the MFA and ATC were limited under quotas but were able to circumvent these restrictions by setting up factories in nearby countries such as Sri Lanka & Bangladesh that had unused capacity under their respective national quotas.These countries operated under the auspices of more established countries such as China seeking to bypass the quota system. As a result, what started as a workaround in places like Vietnam and Cambodia led to the establishment of some of the biggest players in apparel and textiles as deregulation occurred.

When the MFA and ATC eventually did phase out, countries in the developed world with a higher production cost lost a significant cost advantage to their offshore competition.The economic downturn in 2008 reshaped the market even further by allowing exporters that survived the recession to absorb a larger share of the market. Many North American companies were effectively cut out of the industry as their businesses shrank during this consolidation.

That decade following the MFA/ATC phase out was underscored by the recession, and saw billions of dollars annually leaving for offshore manufacturers as textile and apparel manufacturing in developed nations dwindled. Domestic clothing and textile producers typically point out that imported clothing & textiles are being sold below cost,which has led to unemployment as entire sections of the industry have disappeared. Domestic producers lament the flood of cheap imported goods, and accuse the global apparel industry of targeting the North American market with predatory pricing designed to eliminate any remaining competition in the market.

Now a $450 billion dollar business, apparel manufacturing and export is dominated by a range of lesser developed countries bringing a huge variety of competitively priced apparel products to market, thanks to disproportionate labor costs and substandard working conditions. In the absence of regulatory instruments, the apparel and textile industry now represents a significant (if not major) segment of these major players' GDPs.

Shaped by the events of the 1990’s and 2000’s, the major global players in apparel and textile manufacturing established beachheads in the market in the days prior to the MFA/ATC. Many of the former big players from those days were washed out by the 2008-2009 economic crisis, to be replaced by other countries utilized to side step the quota systems of the MFA/ATC.

China, the South Asia Region (SAR) & the South East Asia Region Benchmark (SEAB) top the list of major apparel exporters. SAR includes Bangladesh, Sri Lanka, India & Pakistan, while SEAB includes Vietnam, Indonesia & Cambodia. A recent study shows market share for China, SAR and SEAB were $145 billion, $44 billion & $31 billion, respectively. Some important takeaways to help provide a better understanding of the winners and losers in the apparel export business.

The textile and apparel industry accounts for huge portions of some countries' exports.Some of the countries mentioned above rely heavily on textile and apparel exports, and their governments develop policy to support these industries in an effort to keep these economies competitive. Some measures include reducing import taxes on specific goods to support the industry, or as is the case in China, constructing specialized supply chain cities to streamline production, further enhancing it’s already dominant position in the market. It’s interesting to note that proponents of a free market, especially if that means less government meddling in business quotas or taxes, would be opposed to this form of mass intervention on principle. This point of view argues that the basic rules of economics will balance out any inequalities in the system, but in practice this leaves much to be desired, especially in the form of workers’ rights and respecting the environment.

The free market playbook looks at the apparel market through the lens of basic economic principles. As such, if domestic industries aren’t able to stay competitive, the free market perspective dictates that it’s because the consumer refuses to pay a premium for the more expensive domestic product. Further to this point, if a company is flooding (or “dumping” goods in) a particular market with more goods than there is a demand for, consumers still have a choice to purchase the goods or not. As a side note, this has been happening in practice: huge swathes of inventory left unsold and sent to clearance (or landfill). This guarantees that the consumer will end up with a heavily discounted product, with more cash in their pocket to spend elsewhere in the local economy.

Generally speaking, free market thinking views more affordable goods as a positive, giving the consumer with budget restrictions better value. In the apparel and textile industry, this might impact the domestic manufacturers’ bottom line, cause layoffs for workers in the industry, or even cause the complete offshoring of operations. Despite the immediate downside, this is seen as ultimately healthy for the economy. This is especially true if the alternative is government intervention resulting in tariffs, quotas or subsidized industry, such as increased taxes on imported goods, making both domestic and imported apparel just as expensive for the consumer. This brand of government intervention is the bane of a true free marketeer.

The dominance of SAR, SEAB and particularly China in the modern apparel industry is a stark contrast to the 1990’s before quota systems like the MFA/ATC were phased out. Today, key issues such as workers rights issues haunt labels that rely on imported goods. Additionally, the environmental impact of fast fashion is now top of mind of a consumer increasingly demanding products that are manufactured in a way that respects the environment. These are two evolving factors that show the true cost of an apparel industry run amok.

Both of these factors are explored and unpacked further in the following.

According to the McKinsey & company, the huge carbon footprint of the apparel industry has developed in lockstep with the prevalence of cheap, disposable clothing which has boomed in the last 20 years: The apparel industry has doubled production since 2000, and as of 2014 consumers werepurchasing 60% more clothing and disposing garments twice as fast. The environmental impact of this is exacerbated by the fact that 60% of garments are manufactured with synthetic fabrics such as polyester,which produces 2 to 3 times the carbon emission of cotton to manufacture and does not decompose in landfills. The carbon emissions of the apparel industry could nearly triple by 2050 at current levels of production according to a 2017 report by the Ellen MacArthur foundation.The apparel industry has emerged as one of the heaviest polluters since the mid 1990s, second only to big oil. The current trajectory of the apparel industry is clearly unsustainable.

The $450 billion apparel industry represents the livelihood of hundreds of thousands of people around the world, and is the cornerstone of many countries specializing in textile and apparel manufacturing. Despite this, this industry has long been under the microscope of human rightsgroups due to a vast disparity in wages. A worker in Bangladesh may make as little as $68 a month compared to a wage in China of $230 a month, compared to $1600 a month in the United States.Countries with strong labour laws have not been able to sustain the profitability of their apparel and textile industries due to these global inequalities. As a result, the affordable products consumers purchase domestically come at the cost of poor wages and working conditions for individuals overseas, and lost industries at home.

The shift towards offshore manufacturing combined with increased consumption and pressure by big brands on suppliers to deliver cheaper goods faster has ledto an increase in labour abuse. Long hours, low wages and substandard working conditions are all hallmarks of this industry, not to mention allegations of child labour, non-existant worker compensation and little job security.

Whileproponents of free marketsbelieve that the law of supply and demand will self correct any economic discrepancies, it leaves out the human factor. Government regulations like taxes and quota systems might be seen as unfair economic interference, but current overproduction & rock bottom pricing at the expense of individuals help to justifythese policies. Unions often protect employees in developed countries. Domestic workers expect decent wages and benefits, and a quality of life that is not guaranteed in the countries currently exporting the products we find on our store shelves. Consumers need to decide if the money they save purchasing these imported products is worth the human cost of offshore exploitation and lost jobs at home.

Worker exploitation coupled with over consumption leading to huge portions of product going to landfills, plus the textile and apparel industry becoming a major contributor to global warming, has left consumers more conscious than ever of a brand’s business ethics. This has led to an emerging trend of brands becoming more transparentabout their manufacturing process.

As of 2019, 35% of the 200 brands surveyed had offered full disclosure of their supply chains, up from 12% in 2016. While many brands are still not disclosing, this is a huge shift towards transparency, and offering proofthat brands are becoming aware that respecting human rights is necessary to maintain the trust of consumers.

The current supply chain model could also shift in a big way in the near term, particularly with rising wages in China, which could see a large chunk of their market share heading elsewhere.China is still the largest exporter in this segment, but there is evidence its economy is becoming more diversified. Apparel now accounts for just7% in 2012, compared to 16% in 1990. Those numbers have dropped off again in light of tariffs imposed by the United States.

Rising wages and shifting supply chains coupled with consumers looking to buy from brands that respect both workers and the environment could translate into opportunities for business that are able to deliver and raise the bar on these expectations.The future of this business, like many others, may not lie in the hands of the exporters or the domestic producers, but in the shifting mindset of the consumer.

COVID-19 represents a challenge to industries that rely on a global supply chain including apparel. The 2008-2009 recession might be nothing but a blip compared to the challenges that COVID-19 has brought about, but it is certain that things will not revert immediately back to status quo. Consumer mindset could completely shift towards buying domestically, annihilating the current supply chain and creating a vacuum to be filled by a new range of suppliers ready to step up and shape the new landscape of sustainable fashion.

. .  . .

|